HELPLINE:

HELPLINE:

June closed a turbulent but ultimately constructive first half. Equities digested the spring’s AI-driven rally, the ECB delivered its first rate rise since 2023, and the interim US–Iran agreement signed on 19 June brought oil sharply lower. July opens with a weak US jobs print, markets leaning towards a Fed hold, and — of particular relevance to our cross-border clients — continuing wealth flows between the United Kingdom and France.

MARKETS & MACRO — JUNE 2026 IN REVIEW

Equities

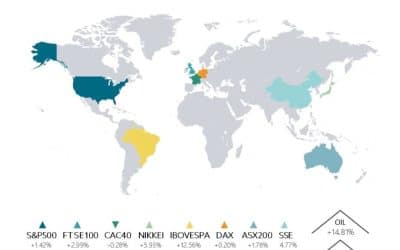

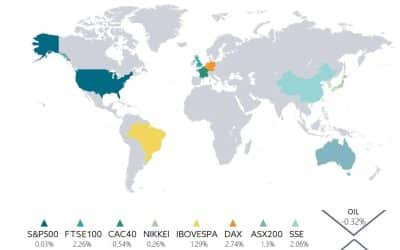

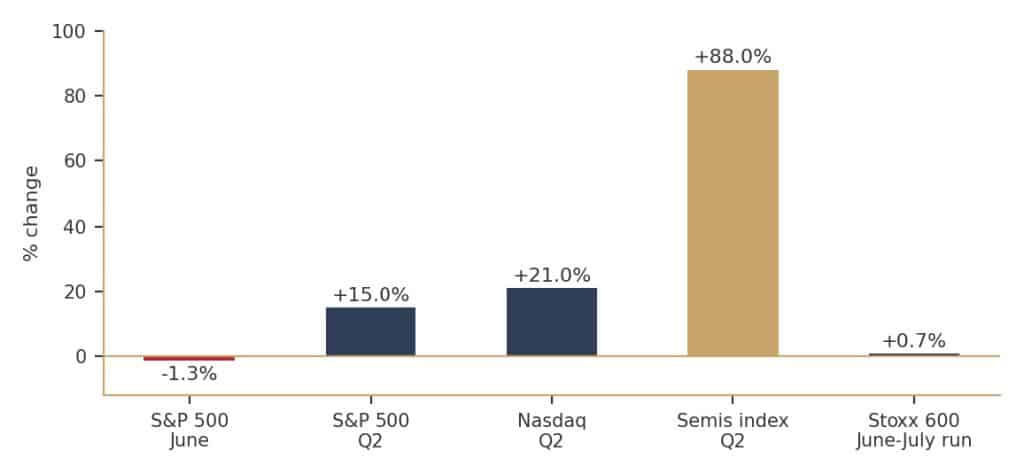

The S&P 500 slipped roughly 1.3% in June to close at 7,499.36, snapping a two-month winning streak after opening the month at a record above 7,600, as investors questioned the pace of the AI rally. The pullback should be seen against an exceptional quarter: the S&P 500 and Nasdaq gained about 15% and 21% respectively since end-March — their best quarter since 2020 — while the semiconductor index surged almost 88%, its strongest quarter on record. Beneath the surface, breadth improved: more S&P 500 constituents ended June above their 50-day average than began it, with weakness concentrated in a handful of mega-cap AI names. Year to date the S&P 500 is up 9.6% and the Nasdaq 12.8%. In Europe, the Stoxx 600 ended the period at a 52-week high after a fourth consecutive weekly gain.

June and Q2 2026 performance. Source: CNN Business, CNBC, FactSet.

Central banks and rates

The ECB raised all three key rates by 25bp on 11 June — its first increase since 2023 — taking the deposit rate to 2.25%, responding to euro-area inflation of 3.2% in May driven by a 10.9% y/y rise in energy prices linked to the Middle East conflict. Eurosystem staff projections now see inflation averaging 3.0% in 2026 and growth of just 0.8%, revised down on war-related effects. The Fed held at 4.25–4.50% in June and signalled patience; Chair Kevin Warsh told the Sintra forum inflation remains “too high” while declining to pre-commit on July. The US 10-year yield ended the period near 4.46%.

Commodities and FX

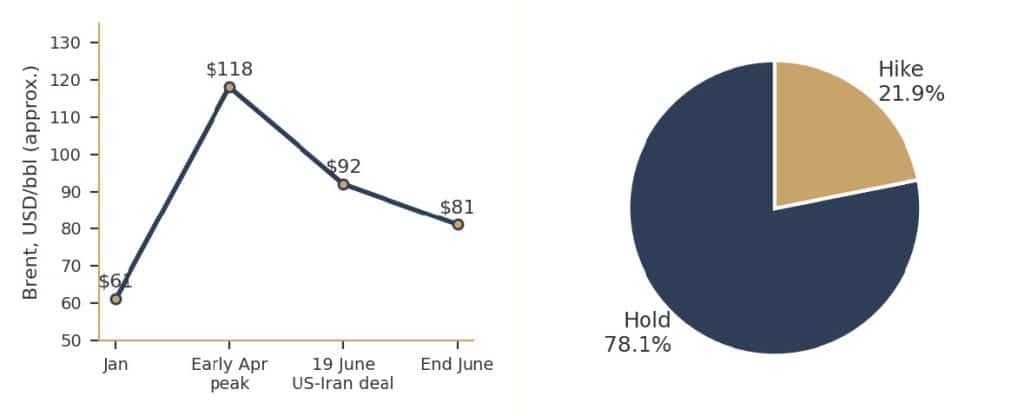

The interim US–Iran agreement signed on 19 June in Switzerland — opening the way to a reopening of the Strait of Hormuz — sent Brent down to around $81/bbl by month-end, some $37 below the early-April peak though still ~$20 above January levels. Gold ended June near $4,100/oz after four consecutive weekly declines, well off its highs but strongly positive for the year. The dollar weakened into month-end – its largest weekly fall since April – with EUR/USD near 1.144.

LEFT: Brent crude through H1 2026, approximate levels. Source: IEA Oil Market Report June 2026, Trading Economics.

RIGHT: July Fed decision, implied probabilities (3 July). Source: CME FedWatch.

PERSPECTIVES FOR JULY

Policy. June US payrolls, released 2 July, rose just 57,000 against 110,000 expected — the weakest in four months — with unemployment at 4.2% on falling participation. Markets price roughly a 78% probability the Fed holds this month; the June FOMC minutes on 8 July are the week’s key event. For the ECB, markets see about a 50% chance of a further hike by September — euro-area inflation and energy prices remain the swing factors.

Geopolitics. Implementation of the US–Iran interim deal and the reopening of Hormuz remain the key variables for oil and inflation. Iran’s leadership transition adds uncertainty: the multi-day funeral of Ayatollah Khamenei is under way while his successor, Mojtaba Khamenei, has yet to appear publicly.

Positioning. With European equities at 52-week highs, a softer dollar and gold stabilising, the month favours discipline over momentum: rebalancing after an exceptional quarter, reviewing duration as rate paths diverge between the Fed and ECB, and revisiting energy-sensitive exposures as the Hormuz normalisation progresses. This is general information, not investment advice; individual positioning should be reviewed with your adviser.

IN FOCUS — UK–FRANCE WEALTH FLOWS: EXPATRIATES AND RETURNEES

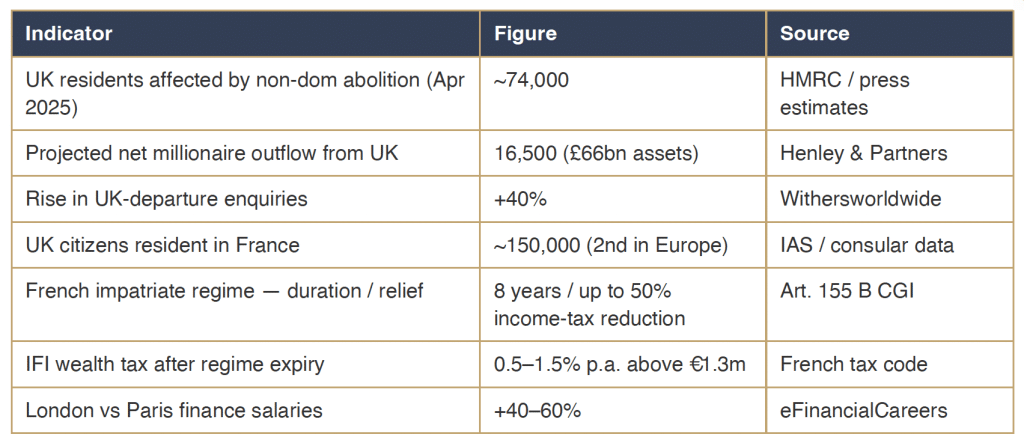

Two migration currents matter for cross-border clients this summer. The first flows out of the United Kingdom: since the abolition of non-dom status on 6 April 2025, affecting an estimated 74,000 residents, Henley & Partners projects a net loss of some 16,500 millionaires from the UK, taking roughly £66bn of investable assets. Withers reports UK-departure enquiries up 40%. Italy has quietly become the preferred jurisdiction for outbound non-doms, but France remains a major destination for British nationals generally — close to 150,000 UK citizens are resident in France, the second-largest British community in Europe after Spain.

The second current is French professionals reassessing their position. Thousands of London-based bankers moved to Paris after Brexit under the impatriate regime (Article 155 B CGI), which offers partial exemptions on salary, foreign income, gains and wealth tax for up to eight years — in practice reductions of up to 50% of French income tax. For the earliest post-Brexit movers those eight years are now expiring: on exit from the regime, worldwide assets above €1.3m fall within the IFI wealth tax (0.5–1.5% p.a.) and marginal income rates can reach 55% including the high-income surtax. Recruiters report early enquiries from Paris-based bankers about a return to London — even as the UK’s own regime has become less generous. Meanwhile London salaries in finance still run 40–60% above Paris levels, keeping the arbitrage alive in both directions.

Key figures, UK–France wealth migration. Compiled from the sources listed.

Advisory note. For clients weighing a move in either direction, timing is decisive: the impatriate regime requires five years of non-residence before (re)establishing French tax residence, exit from the regime should be modelled well before year eight, and UK arrival planning must reflect the post-non-dom four-year FIG regime. Treaty residence, succession exposure (notably French forced heirship) and social-security coordination warrant review before any relocation. This is general information, not tax advice.

WORLD NEWS — JUNE INTO JULY

Iran. Multi-day funeral ceremonies for Ayatollah Khamenei — killed in the opening US–Israeli strikes of 28 February — span five cities in Iran and Iraq before burial in Mashhad on Thursday; the succession remains opaque.

United States. President Trump marked the country’s 250th anniversary with a sharply political Independence Day address.

China. A further military leadership shake-up is read as consolidating Party loyalty.

Pacific. Super Typhoon Bavi struck the Northern Mariana Islands.

World Cup. France advanced past Paraguay 1-0; Mbappé now level with Messi on seven goals.

SOURCES

CNN Business — S&P 500 up almost 10% this year, 1 July 2026: cnn.com/2026/07/01/business/stock-market-up-inflation-war

CNBC — markets coverage, 3 July 2026; Warsh at Sintra, 1 July 2026: cnbc.com

Bloomberg — Stock Market Today, 6 July 2026: bloomberg.com

ECB — Monetary policy decision, 11 June 2026; Eurosystem staff projections, June 2026: ecb.europa.eu

IEA — Oil Market Report, June 2026: iea.org/reports/oil-market-report-june-2026

Trading Economics / CME FedWatch — yields, payrolls, rate probabilities

Henley & Partners — Private Wealth Migration Report (via Cyprus Tax Life, Family Wealth Report)

IAS — Moving to France from UK, 2026 guide: iasservices.org.uk eFinancialCareers — Paris bankers weighing return to London as impatriate benefits expire: efinancialcareers.be

Hayot Expertise / Berton & Associés — French impatriate regime 2026 guides

J.P. Morgan Private Bank — 2026 Global Family Office Report: privatebank.jpmorgan.com

CNN / NBC / NPR / CBS — Iran coverage, 3–5 July 2026