HELPLINE:

HELPLINE: GLOBAL MARKETS DIVERGE AS RISK APPETITE FADES

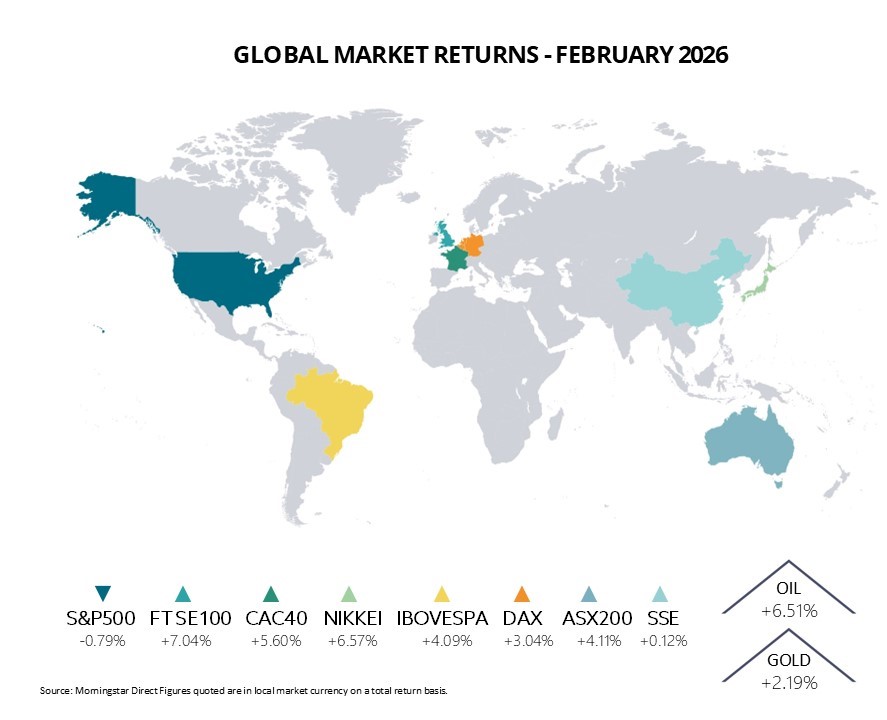

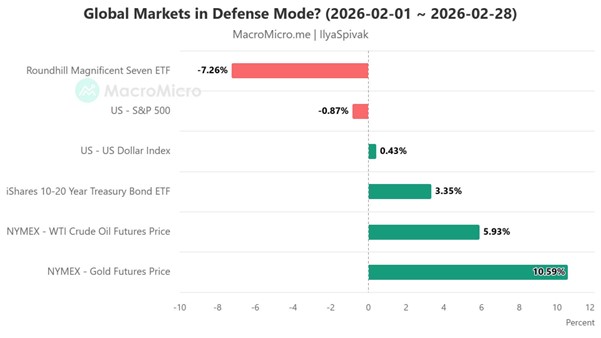

February brought a clear divergence in global equity market performance, as investors began to rein in risk and adopt a more cautious stance toward US technology stocks. Concerns around stretched valuations and a potential existential challenge for software companies drove a retreat from mega-cap names, leading to the S&P 500’s first monthly decline in three months. The index slipped 0.8% in total return terms, while the Nasdaq fell 3.4%, its weakest performance since March 2025.

SPECULATION AROUND POSSIBLE ACTION HELPED PUSH BRENT CRUDE OIL TO A SEVEN-MONTH HIGH EVEN BEFORE THE STRIKES

The US lagged other major markets with Europe’s STOXX 600 delivering an eighth consecutive monthly gain advancing 3.2% to new highs. Japan’s Nikkei posted a stellar 10.4% monthly increase, driven by robust earnings and optimism surrounding the Takaichi administration’s policy agenda. The FTSE 100 broke through the 10,000-point level for the first time, ending the month up 6.7% as energy and financial stocks outperformed.

THE BANK OF ENGLAND HINTED AT THE POSSIBILITY OF THREE CUTS THIS YEAR AS UK INFLATION TRENDS BACK TOWARD 2%

Most markets were closed on 28 February when the US and Israel began striking Iran, meaning the reaction to that escalation will be reflected in March. However, speculation around possible action helped push Brent crude oil to a seven-month high even before the strikes, with supply concerns heightened by tensions in the Strait of Hormuz and increased scrutiny of Russia’s shadow fleet.

It was a strong month across many other asset classes. The 10-year US Treasury yield fell 30 basis points -the largest monthly decline in a year -as risk-off sentiment grew. Meanwhile, gold surged 10.6% to $5,205 an ounce, marking its seventh consecutive monthly gain for the first time since 1973.

On the macro front, mixed signals kept central banks cautious. In the US, producer price inflation surprised to the upside in January at +0.5% month-on-month versus expectations of +0.3%, and core PCE inflation ticked back up to 3%, tempering hopes of an imminent rate cut. Even as markets continued to price in two cuts for 2026, the Fed maintained a wait-and-see approach. Further complication comes from the US Supreme Court’s ruling that restricts the IEEPA tariffs imposed last year.

In contrast, If AI agents can read files, run analyses, and generate outputs autonomously across legal, finance, and sales, the traditional SaaS model comes under pressure, while Eurozone inflation eased to 1.7% in January.

BITCOIN LOSES FAVOUR AS INSTITUTIONS TURN TO GOLD

Bitcoin’s appeal as a hedge against inflation, currency debasement, or equity market stress looks increasingly fragile. Institutional demand has faded for now, with large investors recently favouring gold and other physical assets as safe havens instead.

For much of the past decade, Bitcoin supporters have argued that the largest cryptocurrency is the best protection against currency devaluation and geopolitical shocks. However, when more recently tariff uncertainty and geopolitical tensions have hit traditional markets, safe haven flows have gone into into precious metals rather than crypto. Gold and silver both made new highs during the tariff scare, while Bitcoin dropped sharply, erasing gains and underperforming traditional havens.

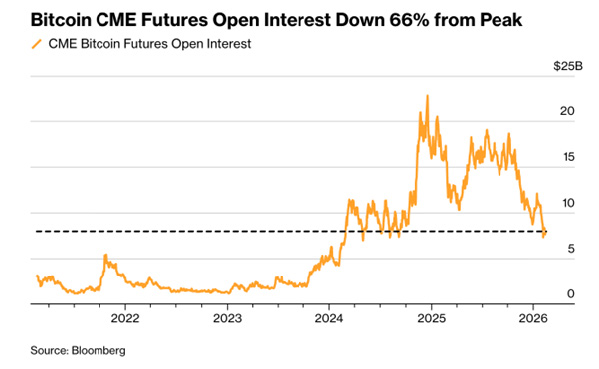

SPOT BITCOIN ETFS, ONCE THE FLAGSHIP OF INSTITUTIONAL ADOPTION, HAVE SEEN AROUND 9 BILLION DOLLARS OF OUTFLOWS SINCE OCTOBER

Within crypto, Bitcoin is no longer the undisputed leader. Yield generating DeFi protocols and tokenised real world assets now compete for capital seeking income or clear utility, while Bitcoin offers neither cash flow nor commodity like industrial use. Correlations with several large alt coins such as Dogecoin and Cardano have loosened, suggesting a more fragmented market structure rather than investors consolidating around Bitcoin as a single, dominant macro hedge. Spot Bitcoin ETFs, once the flagship of institutional adoption, have seen around 9 billion dollars of outflows since October, and CME futures positioning has dropped by roughly two thirds from late 2024 highs, signalling a retreat of “fast money” from the macro hedge trade.

SOFTWARE BUSINESS MODELS UNDER AI PRESSURE

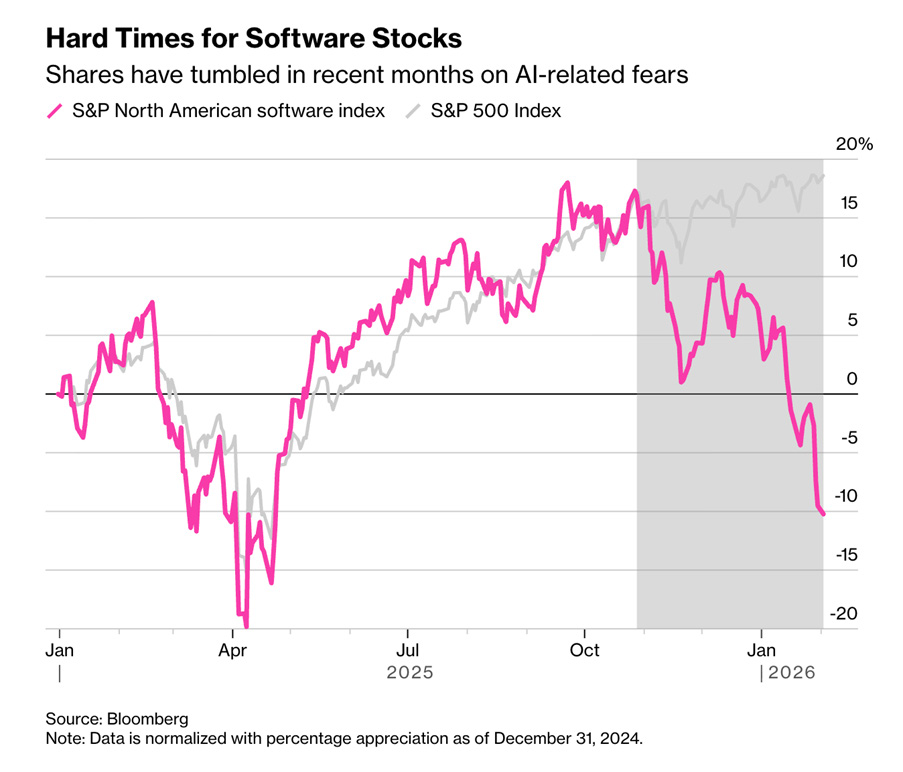

Software and software as a service (SaaS) stocks have been sharply repriced as investors reassess how AI driven automation and potential job losses could undermine the sector’s core business model. In just a few days between late January and early February, about $285 bn of market value was wiped out across software, legal tech, and data service names, in what traders dubbed the “SaaSpocalypse,” with a key Goldman Sachs software basket falling roughly 15% and ending around 25% below its recent peak.

IN JUST A FEW DAYS BETWEEN LATE JANUARY AND EARLY FEBRUARY, ABOUT $285 BN OF MARKET VALUE WAS WIPED OUT ACROSS SOFTWARE, LEGAL TECH, AND DATA SERVICE NAMES

High profile names were hit hard. Adobe dropped close to 20% over the month, while information services and legal software providers such as Thomson Reuters and peers in legal and compliance workflows suffered double digit year to date declines, as Anthropic’s new “Claude Cowork” plugins stoked fears that large parts of their value proposition could be automated away.

If AI agents can read files, run analyses, and generate outputs autonomously across legal, finance, and sales, the traditional per seat SaaS model – built on human users logging in and doing work – comes under pressure as decisions tilt toward in house AI systems.

There is, however, a growing view that the selloff has overshot fundamentals and that AI will rely on and enhance software tools rather than replace them. Several venture and public market investors contend that while some incumbents will be disrupted and pricing models will change, SaaS is more likely to evolve than vanish, because customers still need secure, governed, domain specific applications wrapped around general purpose models.

IF AI AGENTS CAN READ FILES, RUN ANALYSES, AND GENERATE OUTPUTS AUTONOMOUSLY ACROSS LEGAL, FINANCE, AND SALES, THE TRADITIONAL SAAS MODEL COMES UNDER PRESSURE

The sector had been inflated in a zero interest rate era and expectations of endless expansion, so part of this year’s drawdown looks like a long overdue correction even as AI disruption forces a more sober view of future growth. Ultimately, survival for software and SaaS companies will depend on proving that their products deliver real, defensible value in an AI first world – via distinctive data, deep workflows, strong governance, or automation that customers cannot cheaply replicate.