HELPLINE:

HELPLINE: VOLATILITY IN COMMODITIES AS GEOPOLITICS DRIVES RETURNS

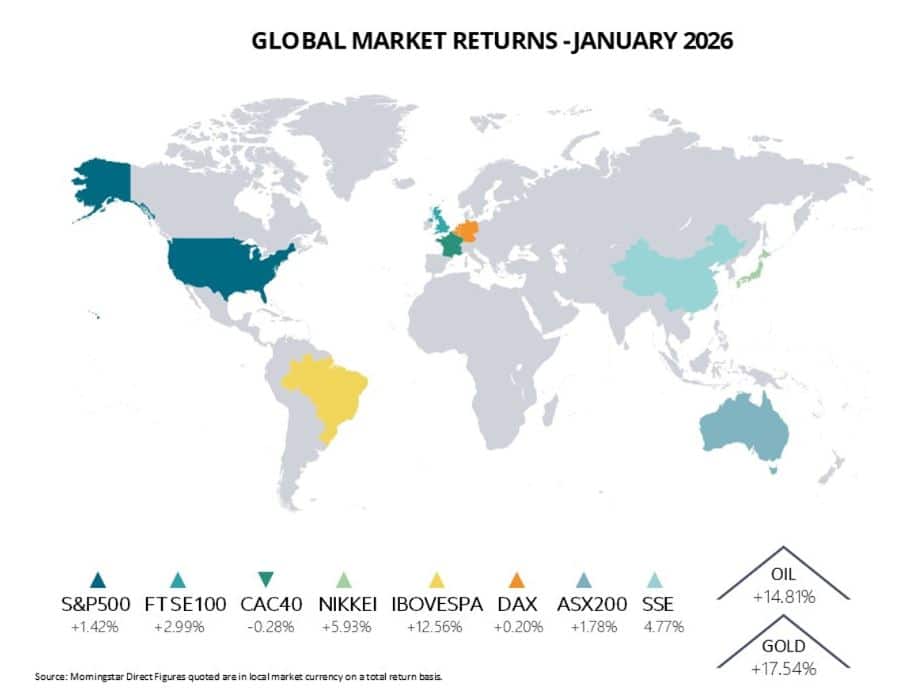

January brought continued positive data surprises and most markets produced positive returns; however, as in 2025, headline gains came despite mounting geopolitical risks, including tensions around Venezuela, Iran, and Greenland. These concerns were supportive for commodity prices and helped Brent Crude (+16%) achieve its largest monthly gain in four years after President Trump warned that a “massive Armada” was heading to Iran, prompting speculation about a possible US strike. Precious metals registered their strongest advance in decades, with the gold price (+13%) seeing its biggest monthly increase since September 1999, despite a sharp pullback at the end of the month.

All this occurred alongside growing pressure on the US dollar, which suffered its largest 4-day fall since the “Liberation Day” turmoil last year, weakening against every other G10 currency in January. In the first half of the month, financial markets extended the positive momentum that had carried over from 2025, with risk assets rallying on dollar weakness and earnings optimism. However, the month ended with news of Trump’s nomination of Kevin Warsh for Fed chair, which triggered a sharp reversal in commodities and reminded investors that volatility remains an important feature under the Trump administration.

BRAZIL’S BOVESPA INDEX GAINED 13%, ITS BEST MONTH SINCE NOVEMBER 2020

Emerging markets delivered their strongest January performance since 2012. The MSCI Emerging Markets Index rose almost 9% for the month, reaching historical highs. The rally was not primarily driven by China, where performance was mixed amid regulatory shifts and moderating growth data. Instead, gains reflected broad-based strength across developing economies and improving fundamentals. Brazil’s Bovespa index gained 13%, its best month since November 2020, while emerging market currencies generally appreciated.

As investors continue to diversify away from US assets, European equities extended their winning streak. The European STOXX 600 produced a seventh consecutive monthly advance, supported by stronger corporate earnings and strength from more defensive sectors. The UK FTSE 100 gained over 2%. In Japan, the Nikkei Index ended up almost 6%. The S&P 500 and Nasdaq produced modest positive returns in USD terms, but negative returns for most foreign investors after currency translation.

The Warsh Fed nomination triggered sharp moves across many asset classes. The dollar recorded its strongest day since May last year, while precious metals experienced their worst single-day decline since 1980. Gold fell 11%, and silver dropped 31%, as the prospect of a less accommodative Fed weighed on the safe-haven trade that had driven metals to record highs.

Cryptocurrencies struggled in the risk-off phase, with Bitcoin and other major digital assets trending lower as speculation about US rate policy reduced appetite for more speculative exposures. Despite the late-month turbulence, the broader themes from 2025 remain largely intact, with diversification continuing to be a priority beyond US technology stocks.

JAPAN – A GENUINE CHANGE OF DIRECTION?

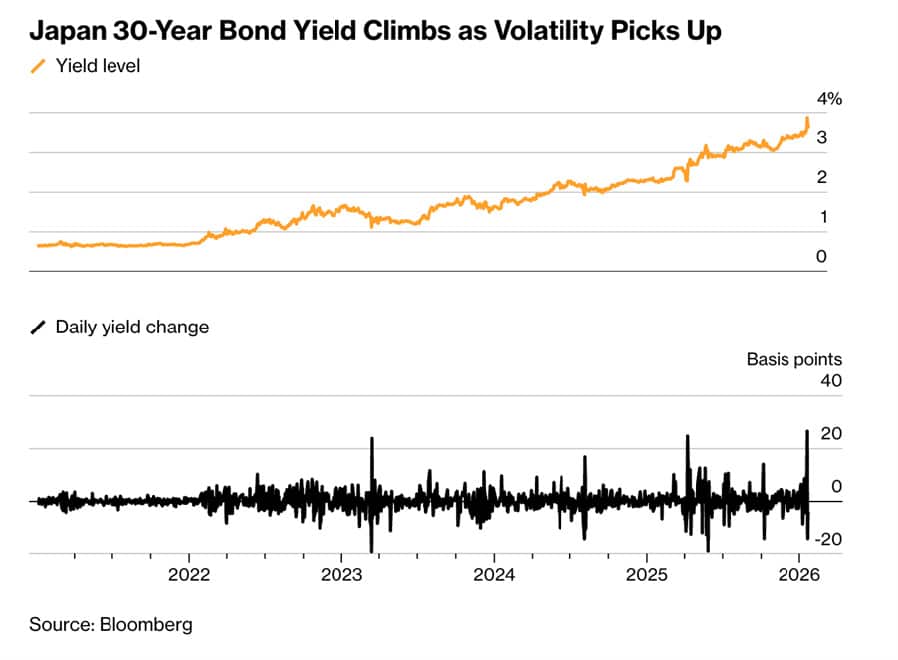

There is an increasing focus on Japanese financial markets and questions about whether Japan’s decades-long period of ultra-low rates and heavy monetary accommodation is beginning to shift. January brought a sell-off in Japanese government bonds (JGBs), high yen volatility, and renewed scrutiny of the global carry trade.

The JGB market saw yields rising at a pace rarely seen in Japan’s traditionally stable bond market. Thirty- and forty-year JGB yields moved to multi-decade highs above 4%, with the 30-year yield climbing more than 25 basis points in a single day, around eight times the average daily range of the previous five years.

WITH GOVERNMENT DEBT ALREADY ABOVE 230% OF GDP, THE HIGHEST AMONG G7 ECONOMIES, MARKETS ARE BEGINNING TO RE-EVALUATE THE RISK PREMIUM ON JAPANESE SOVEREIGNS

These moves reflect growing concern about Japan’s fiscal trajectory under Prime Minister Sanae Takaichi, whose stimulus proposals and snap election call for 8 February have heightened focus on debt sustainability. With government debt already above 230% of GDP, the highest among G7 economies, markets are beginning to re-evaluate the risk premium on Japanese sovereigns after many years of relative stability.

Currency markets have amplified these dynamics. The yen weakened sharply early in January, approaching historic lows near ¥160 against the dollar, before reversing following signals of coordinated action from Japanese and US authorities. The Federal Reserve Bank of New York conducted rate checks at the direction of Treasury Secretary Scott Bessent, who expressed concern about potential spillovers from JGB volatility into US Treasury markets, highlighting how developments in Japan have become relevant for global fixed-income conditions.

THE YEN WEAKENED SHARPLY EARLY IN JANUARY, APPROACHING HISTORIC LOWS NEAR ¥160 AGAINST THE DOLLAR

These moves have significant implications for the yen carry trade, a strategy that has channelled hundreds of billions of dollars into global risk assets over several decades by exploiting Japan’s low borrowing costs. Rising JGB yields and higher currency volatility are reducing the attractiveness of this trade and increasing the risk of a more disorderly unwind, as yield differentials between Japan and major economies narrow. Japanese institutions, including large banks and insurers, have signalled plans to repatriate capital and rebuild domestic JGB holdings, which could gradually reduce liquidity in some global markets. The Bank of Japan has kept its policy rate at 0.75% but has begun to taper bond purchases. Global investors can no longer treat Japan as a consistently stable source of low-cost funding. Whether these changes are permanent or transitory remains to be seen.

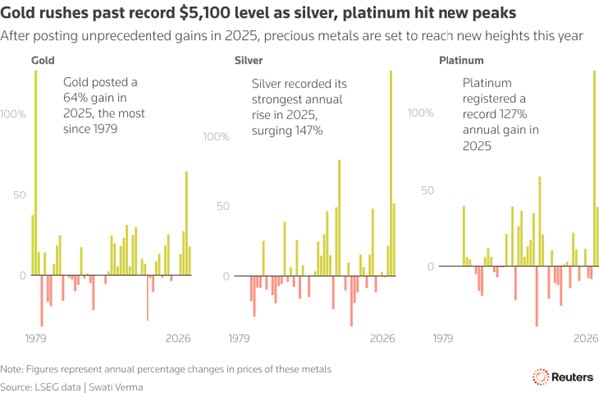

PRECIOUS METALS – A HISTORIC MONTH, NOT JUST A HEADLINE CRASH

January 2026 was among the most volatile months on record for precious metals, combining a historic rally with a sharp late-month correction. The complex as a whole saw both record highs and rapid drawdowns, demonstrating how liquidity, positioning and policy expectations can interact in tightly traded markets.

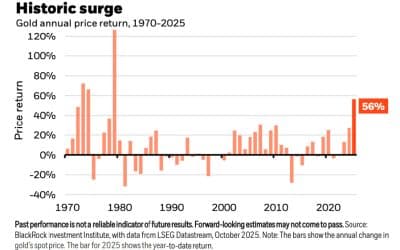

For most of the month, gold, silver, platinum and palladium moved sharply higher. Gold extended its multi-year bull market, breaking above $5,000 an ounce and briefly trading around $5,500, representing more than a 90% increase over the past 12 months. Silver’s move was even more pronounced, and prices broke through $100 an ounce for the first time and even exceeded $120, implying annual gains close to 300% at the peak. Platinum reached record levels near $2,900, and palladium advanced to its highest level in several years.

THE CME GROUP RAISED MARGIN REQUIREMENTS ON COMEX GOLD AND SILVER FUTURES, COMPELLING LEVERAGED TRADERS TO POST ADDITIONAL CAPITAL

The rally reflected a combination of factors including structural supply deficits in some metals, robust industrial demand, safe-haven inflows amid heightened geopolitical uncertainty, and technical drivers such as short-covering as traders closed out bearish positions. Strong central-bank buying and expectations of easier US monetary policy in 2025 had already set the stage for elevated prices going into the new year.

In the final days of January, however, there was a pronounced correction. Gold recorded its sharpest daily decline since the early 1980s, while silver saw one of its largest intraday drops on record, with futures falling by more than 30% in a single session. The shift coincided with the announcement that Kevin Warsh would be the next US Federal Reserve chair, signalling a potentially less dovish stance.

ONE OF THE MOST VOLATILE MONTHS ON RECORD FOR PRECIOUS METALS SAW GOLD, SILVER AND PLATINUM REACH RECORD LEVELS BEFORE A PRONOUNCED LATE-MONTH CORRECTION

Market structure played a central role in the speed and scale of the decline. The CME Group raised margin requirements on Comex gold and silver futures, compelling leveraged traders to post additional capital or reduce exposures. This contributed to forced selling and a self-reinforcing move lower, particularly in silver.

Looking ahead, the recent price action does not necessarily alter the longer-term positive case. Many of the factors that supported the rally remain in place. However, the January experience demonstrates the importance of sizing positions appropriately and being prepared for periods in which technical and liquidity factors dominate fundamentals.